Which loan is better, USDA or FHA?

When it comes to USDA vs FHA, it all depends on your situation.

USDA loans allow no down payment and have cheap mortgage insurance, but you have to buy in a “rural” area and meet income limits. FHA loans are more flexible about income, credit, and location, but they can have higher costs.

Check your home loan options. Start hereLuckily, there’s an easy way to choose. Just ask your lender about USDA loans and FHA loans. You might be eligible for one but not the other. If you’re eligible for both, you can compare rates and fees to see which loan option is better for you.

In this article (Skip to…)

USDA vs FHA loan: An overview of differences

The choice between USDA and FHA loans is often pretty easy since they’re targeted at different types of buyers.

Check your home loan options. Start hereThe USDA loan program is meant to make homeownership more accessible in lower-income rural areas. Only certain locations qualify, and you have to be within income limits to apply.

The FHA loan program is more widely available. Buyers can apply in any part of the country, and there are no income restrictions to qualify. But what sets the FHA program apart in a USDA vs FHA comparison is its lenient credit score requirements. Home buyers can apply with a FICO score of just 580 and 3.5% down. For this reason, FHA loans are usually recommended for borrowers with credit scores too low to qualify for a standard conforming mortgage loan.

USDA vs FHA: Eligibility

A large part of the decision between USDA vs FHA loans will depend on which type of mortgage you qualify for. Here’s a brief overview of how USDA and FHA eligibility requirements compare.

Check your home loan options. Start here| Criteria | FHA Loans | USDA Loans |

| Loan Requirements | Minimum credit score of 580 for 3.5% down payment Steady employment history Property must be primary residence | Must meet income eligibility Property must be in a USDA eligible area Property must be primary residence |

| Loan Limits | Vary by county, but typically up to $ for single-family homes in most areas | No set loan limit, but the home must be modest in size for the area, and cannot have luxury features |

| Income Limits | None | Usually 115% of area median income (AMI) |

| Appraisal | Required Must meet HUD's minimum property standards | Required Must meet USDA's property and location requirements |

| Down Payment | Minimum of 3.5% with a credit score of 580 or higher 10% for credit scores between 500-579 | No down payment required |

| Mortgage Insurance | Upfront mortgage insurance premium (1.75% of the loan amount) Annual mortgage insurance premium (0.45% to 1.05% of the loan amount, paid monthly) | Upfront guarantee fee (1% of the loan amount) Annual fee (0.35% of the loan amount, paid monthly) |

| Interest Rates | Vary by lender, credit score, down payment, and other factors Typically lower for borrowers with good credit | Set by the lender, but can be as low as current market rates due to government backing |

| Closing Costs | Vary by lender, but can include appraisal fees, credit report fees, lender's origination fees, etc. Can be covered by seller or lender | Can include appraisal fees, credit report fees, lender's origination fees, etc. Can be rolled into the loan amount or paid by the seller |

The FHA program offers 30-year and 15-year fixed-rate mortgages, along with adjustable-rate mortgages (ARMs). The USDA offers only a 30-year fixed-rate loan.

In addition, both programs require you to buy a primary residence, meaning you can’t use them for a vacation home or investment property. However, FHA loans can finance multi-family homes with 2, 3, or 4 units, whereas a USDA loan can be used only for a single-family home.

Differences between USDA and FHA loans

When comparing USDA vs FHA loans, both government-backed, differences emerge in terms of application, underwriting, appraisal, loan amounts, mortgage insurance, interest rates, and more. Prospective borrowers often wonder, “Is USDA better than FHA?” To answer this, it’s essential to carefully analyze the details of USDA vs FHA loans to make an informed decision based on their specific financial circumstances and homeownership aspirations.

Check your home loan options. Start hereApplication process and underwriting

The journey to homeownership begins with preapproval, regardless of whether you opt for a USDA or FHA loan. Preapproval signals to sellers that you’re serious about purchasing and likely to secure a mortgage.

Prequalification is another option where the mortgage lender makes a decision based on the information you provide. However, preapproval involves a more thorough check, including a credit history report and documentation like tax documents and pay stubs.

One big difference between USDA and FHA is that the USDA home loan process might take longer than an FHA loan, as USDA loans undergo double underwriting—first by the lender, then by the USDA. Automatic underwriting by the USDA requires a credit score of 640 or higher. Manual underwriting, which extends the loan closing time, is for those with scores below 640. A USDA loan typically closes in 30 to 45 days.

An FHA loan also takes about 30 to 45 days to close, depending on the application process and underwriting duration. The application and origination phases may take 1–5 business days. Processing and underwriting times also depend on how promptly you provide the necessary documentation.

Loan limits

FHA loans have maximum loan limits set by the Department of Housing and Urban Development (HUD). In 2025, the maximum FHA baseline limit was set to $. Caps are even higher in areas with expensive real estate, where FHA loan limits now reach well above $1 million.

USDA loans, in contrast, don’t have set loan limits. The maximum amount is determined based on your eligibility for a USDA loan.

Appraisal

Understanding the appraisal requirements is critical when comparing USDA loan vs FHA loan options. It ensures the house is sold at fair market value. For a USDA loan, the appraiser must confirm the property is in a USDA-determined rural area and is habitable. For an FHA loan, the appraiser must ensure the home meets health and safety standards set by the Department of Housing and Urban Development (HUD).

Down payment

FHA loans require a down payment of 3.5% if your credit score is 580 or higher and 10% for a credit score range of 500–579. USDA loans, however, do not require a down payment.

Mortgage insurance

Both USDA and FHA loans require mortgage insurance. FHA loans require a monthly mortgage insurance premium (MIP) for the entire term of your mortgage unless you make a down payment of 10% or more. In that case, MIP comes off after 11 years.

USDA home loans require a guarantee fee, paid at closing and monthly throughout the loan term. The upfront fee is 1% of the full loan amount, and the monthly premium is 0.35% of the unpaid principal balance of your USDA loan.

Interest rates

When it comes to USDA vs FHA interest rates, both loans typically offer lower interest rates due to government backing. However, the mortgage insurance requirement could make both USDA and FHA loans more expensive over the loan’s lifespan.

Closing costs

For both loans, whether it’s USDA vs FHA, the buyer may need to cover the loan’s closing costs. The difference between FHA and USDA loans is that with USDA loans, a borrower can finance up to 100% of a home’s appraised value, and the excess funds can be used for closing costs. You could also negotiate for seller concessions to cover up to 6% of your closing costs for either loan.

Find the right mortgage for you. Start here

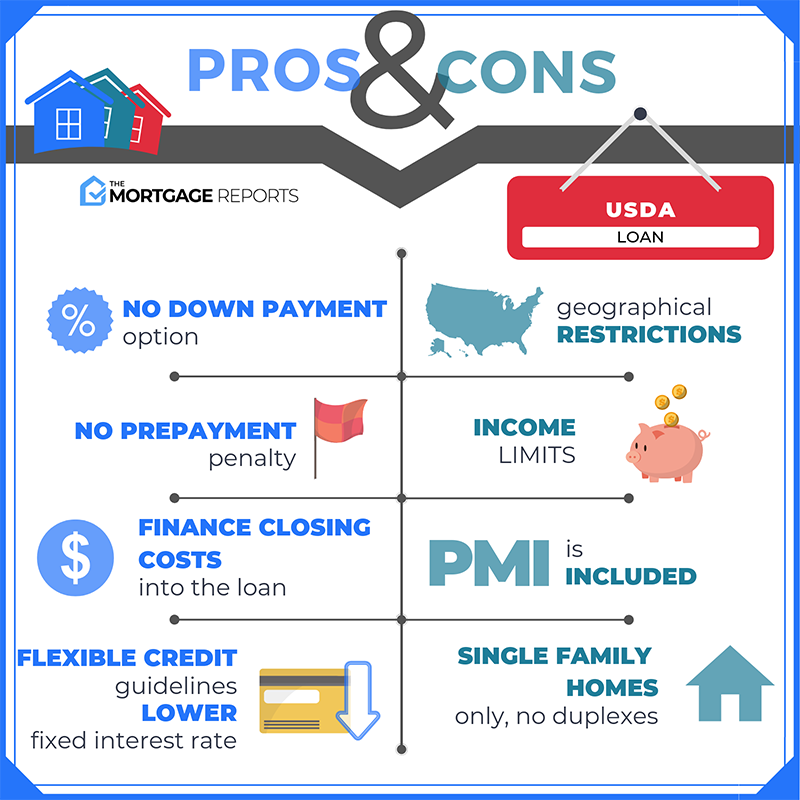

Pros and cons of USDA loans

The USDA loan has quickly risen in popularity with first-time and lower-income borrowers thanks to its zero-down allowance and low rates. But not everyone will qualify. Here’s what you should know.

Check your home loan options. Start here

Pro: Zero down payment required

When comparing USDA vs FHA, USDA loans stand out for their zero down payment requirement. You may finance up to 100% of the property value, which, sometimes, is above the home’s purchase price. In these cases, the buyer can finance closing costs.

For example, say you make an offer on a home for $200,000. The lender’s official appraisal report states the home is worth $205,000. The buyer can open a USDA loan for the full value, as long as the excess funds are applied to closing costs such as the title report, loan origination fees, homeowner’s insurance, and prepaying property taxes and homeowner’s insurance.

So, in the end, USDA borrowers could get into a home with close to nothing out of pocket.

The difference between USDA and FHA is that with FHA, the home buyer must come up with a 3.5% down payment plus closing costs. The FHA has no guidelines stating that the loan amount can exceed the purchase price. The only way to get a zero-out-of-pocket loan with FHA is to get a substantial down payment gift, down payment assistance, or seller contributions for closing costs.

The USDA is more flexible, and buyers with little cash on hand should look into this option first.

Con: You must buy in a rural location

USDA eligibility depends on the location of the home. You must purchase a property in a rural area as the USDA defines it. But the definition of “rural” is quite liberal, and it’s based on U.S. census information from more than 15 years ago. So many suburban areas are still eligible.

USDA publishes online maps that buyers can use to check the eligibility of a certain address or geographical area. Buyers will find that some entire states are USDA-eligible. Even highly populated states contain surprisingly vast qualifying areas. An estimated 97% of the American landscape is geographically eligible for a USDA loan.

Still, some buyers might find that eligible areas are too far outside employment centers and, for that reason, choose an FHA loan, which comes with no geographical restrictions.

Con: Income limits apply

The Rural Development Loan was created to spur homeownership in rural areas, especially among low- and moderate-income home buyers who might not otherwise qualify.

As such, the USDA publishes income limits. Maximums are set at 115% of the median income for your county or area. But these limits aren’t overly restrictive. The following are examples of maximum household incomes in various locales around the country:

- Denver, Colorado: $114,850

- Portland, Oregon: $91,900

- Philadelphia, Pennsylvania: $111,100

- Albany County, Wyoming: $93,750

You can find the current USDA income requirements for your area here.

Not everyone will fall within the USDA income limits. That’s where FHA comes in. FHA loans come with absolutely no income limits for their standard program.

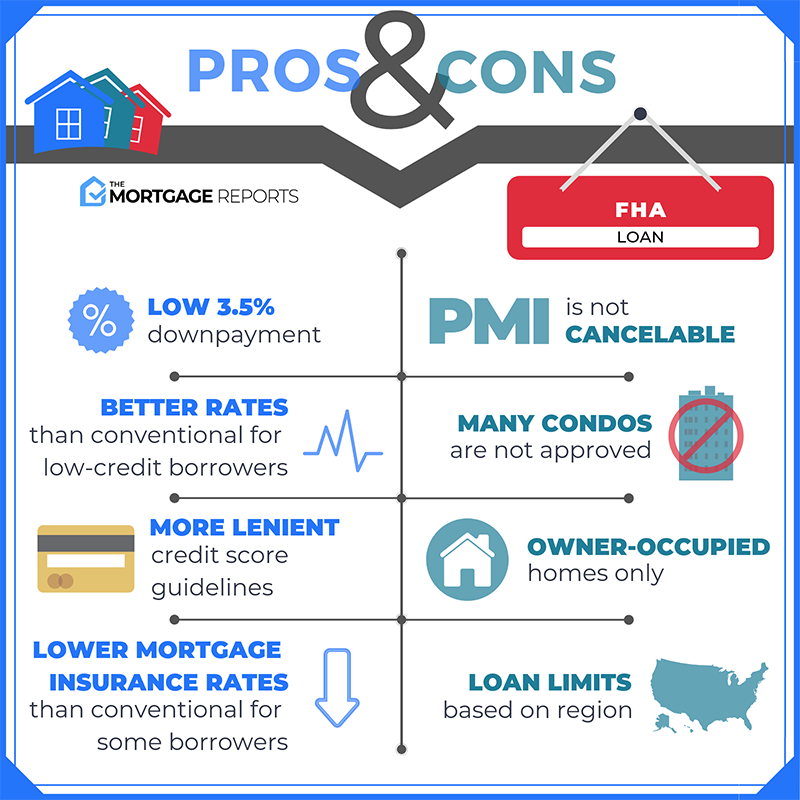

Pros and cons of FHA loans

While USDA loans stand out for being ultra-affordable, many borrowers prefer an FHA mortgage for its looser underwriting requirements.

Check your home loan options. Start hereThere are no income limits for an FHA loan, and you might be able to get away with a lower credit score and higher debts than USDA or conventional lenders would allow. Here’s what you should know.

Pro: Flexible credit requirements

For those with lower credit scores, the FHA loan might be more attractive in the USDA vs FHA loan comparison.

Most FHA lenders will accept credit scores as low as 580 with just 3.5% down. That’s a far cry from the USDA’s 640 credit minimum. The Federal Housing Administration will even allow FICO scores of 500–579. However, you’ll need to make a 10% down payment, and few lenders will actually approve scores this low.

FHA tends to be flexible when it comes to credit history, too. For example, FHA guidelines specifically state that a lack of credit history is not a reason to deny someone’s mortgage loan application.

If you have very little information on your credit report—or none at all—because you haven’t borrowed much in the past, an FHA loan is still an option. You’ll just have to prove your financial responsibility in another way, for example, with a 12-month history of on-time rent payments.

The USDA has similar rules, but it might be harder to find a USDA lender to approve you. With the FHA program, lenient credit requirements are the norm.

Pro: Flexible debt-to-income ratios

FHA is also more flexible than USDA when it comes to debt-to-income ratios (DTI), which is a significant factor in the USDA vs FHA comparison.

Your debt-to-income ratio compares your monthly debt payments to your gross monthly income. Lenders use this number to determine how much of your income is taken up by existing debts and how much room is left over in your budget for monthly mortgage payments.

Although the U.S. Department of Agriculture doesn’t set loan limits, its income limits effectively cap the amount you can borrow. For instance, if your monthly pre-tax income is $4,000 and you pay $600 per month toward student loans and credit cards, your existing DTI is 15%.

USDA’s maximum DTI, including housing payments, is typically 41%. So the most you can spend on your mortgage each month is $1,040.

- $600 + $1,040 = $1,640

- $1,640 / $4,000 = 0.41

- DTI = 41%

The USDA typically limits debt-to-income ratios to 41%, except when the borrower has a credit score over 660, stable employment, or can demonstrate a demonstrated ability to save. These mortgage application strengths are often referred to as “compensating factors" and can play a big role in getting approved for any mortgage, not just USDA.

FHA, on the other hand, often allows a DTI of up to 45% without any compensating factors. In the example above, a 45% DTI allowance raises your maximum mortgage payment to $1,300. A higher monthly payment increases the amount you can borrow. That means you can potentially buy a better, more expensive home.

If existing debts are an issue for you, you may want to choose an FHA loan over a USDA loan for its flexibility in this area.

Con: Higher mortgage insurance rates

The main downside to FHA financing is that you pay mortgage insurance premiums (MIP).

Both FHA and USDA loans require borrowers to pay mortgage insurance. So do conventional mortgage loans when buyers put less than 20% down. This is known as private mortgage insurance, or “PMI.”

All three kinds of mortgage insurance protect the lender in the event of foreclosure. USDA’s mortgage insurance rates are typically the cheapest of the three.

On the other hand, FHA loans are known for having more expensive mortgage insurance premiums. Although conventional PMI rates might actually be higher if you have a lower credit score and a small down payment.

Take a look at how mortgage insurance costs might compare for a $250,000 home with 3.5% down. The borrower in this scenario has a 640 credit score.

| USDA Mortgage Insurance (MI) | FHA Mortgage Insurance Premium (MIP) | Conventional Private Mortgage Insurance (PMI) | |

| Upfront Fee (% of loan amount) | 1.0% | 1.75% | None |

| Upfront Fee ($) | $2,400 | $4,200 | $0 |

| Annual Rate (% of loan amount) | 0.35% | 0.55% | 1.65% |

| Monthly Payment (annual rate / 12) | $70 a month | $111 a month | $330 a month |

A few things to note here:

- Upfront mortgage insurance premiums for USDA and FHA can be rolled into the loan amount

- Conventional PMI rates can drop steeply when you have a higher credit score

Another difference between FHA vs USDA vs conventional is that when it comes to mortgage insurance, a conventional PMI can be canceled once a homeowner has at least 20% equity.

By contrast, USDA mortgage insurance lasts the life of the loan. So does FHA mortgage insurance, unless you put at least 10% down. In that case, MIP lasts 11 years. While this might seem like a deal-breaker, even homeowners with “permanent” mortgage insurance aren’t stuck with it forever.

Those with FHA and USDA loans may be able to refinance into a conventional loan with no PMI once they reach 20% equity in the home. So, if you have a credit score in the low 600s and PMI rates are super high, don’t let the fact that PMI is cancelable sway you. An FHA or USDA loan could still be cheaper in the long run.

How to choose between USDA vs FHA loans

USDA and FHA loans are both government-backed mortgages. The Federal Housing Administration backs FHA loans, while the U.S. Department of Agriculture guarantees USDA loans.

Check your FHA loan eligibility. Start hereNeither of these government agencies directly underwrites home loans. Instead, they provide protection to lenders in case borrowers default on their mortgages. This guarantee allows lenders to offer flexible eligibility requirements and lower interest rates, too.

What does that mean for you? A few things:

- Loan requirements are easier for FHA and USDA loans thanks to their government insurance

- Both loan types charge upfront and annual mortgage insurance to fund the programs

- Both USDA and FHA loans are available from major nationwide lenders

- Mortgage interest rates for FHA and USDA are competitive

Both USDA and FHA are great first-time home buyer loans thanks to their flexible guidelines and low upfront costs.

However, the main downside to both programs is that you’ll pay ongoing mortgage insurance fees that cannot be canceled. To get out of USDA or FHA mortgage insurance, you’d have to refinance your mortgage later on.

FAQ: USDA vs FHA loans

When considering USDA vs FHA loans, determining which one is better relies on your specific financial situation. Buyers with lower credit scores will likely discover that FHA loans suit their needs best. On the other hand, home buyers may find the USDA loan attractive if they seek a cheaper loan without any down payment requirements. Ultimately, the decision between USDA vs FHA loans hinges on a buyer’s priorities and personal finances.

USDA loans are typically regarded as being cheaper than FHA loans. In a USDA loan vs FHA loan comparison, USDA loans have no down payment requirements and lower mortgage insurance premiums.

One of the primary differences between USDA and FHA loans is the geographic restriction of USDA loans. A USDA loan is only available to buyers who are purchasing a primary residence in a designated rural area. Even though an estimated 97% of the U.S. is eligible, buyers who need to live near employment centers or larger metro areas will likely need to consider an FHA or conventional mortgage loan.

Both USDA and FHA loans are backed by government agencies that protect lenders in the event of default. Additionally, both are fixed-rate loans that are available to home buyers who may have difficulty qualifying for a conventional loan.

When comparing mortgage options, such as USDA vs FHA loans, the better choice largely hinges on one’s financial situation. For instance, individuals with lower credit scores may discover that FHA loans suit their needs best. On the other hand, those seeking a more cost-effective loan without any down payment requirements might find the USDA loan attractive. Ultimately, the decision between USDA vs FHA loans boils down to a buyer’s priorities and personal finances.

Compare USDA vs FHA mortgage rates

Ready to dive into the world of real estate with the confidence of a well-informed buyer?

Whether you’re eyeing USDA, FHA, or veteran-friendly VA loans, the key to unlocking the best deal is comparison.

Don’t just dream about your perfect home — own it! Click below to compare rate quotes from top lenders and start your journey to homeownership with the best rates in your pocket.

Time to make a move? Let us find the right mortgage for you