Will mortgage rates go down in 2023?

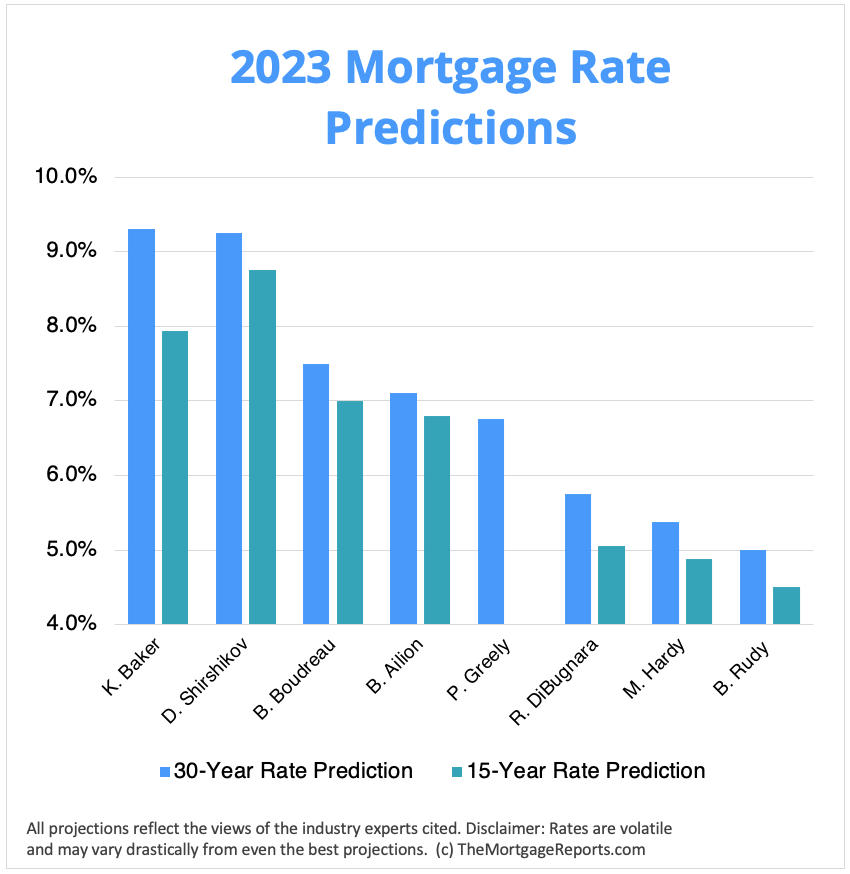

We polled eight industry insiders for their 2023 mortgage rate predictions and answers varied widely, from just 5% to over 9% for the 30-year fixed rate.

Mortgage rates rose steadily in 2022 before falling substantially from mid-November through December. If that trend continues, we could see 2023 mortgage rates nearing the low end of those predictions — around 5%-6%.

Experts tend to agree that continued high inflation will keep mortgage rates around their current levels, while it would take a recession or an unexpected “black swan event” to push them much lower.

Find your lowest mortgage rate. Start hereIn this article (Skip to...)

How high will mortgage rates go in 2023?

The experts we polled expect average 30-year mortgage rates to land anywhere between 5.0% and 9.31% in 2023 — a huge potential range. Predictions fall between 4.5% and 8.75% for the 15-year fixed mortgage rate.

Averaged together, mortgage rate forecasts call for 30-year fixed rates at 7.0% and 15-year fixed rates at 6.42% in 2023. But a number of factors could lead to unexpected rate movements in the coming year.

Climbing inflation, aggressive Federal Reserve policies, the war in Ukraine, and fears of an impending recession have all muddled the current economic climate, making mortgage rate movements incredibly hard to predict. As always, mortgage pros recommend buying a home when you’re financially ready and can afford it, rather than trying to time the market.

With rate movements so unpredictable, waiting on borrowing costs to fall could just as easily lead to higher rates. And keep in mind that if you buy now, you’ll likely have opportunities to refinance into a lower rate later on — whether in 2023 or a couple of years down the line.

Find your lowest mortgage rate. Start here

What's causing mortgage rates to rise?

A number of factors caused mortgage interest rates to shoot up in 2022 — and these trends seem likely to continue well into 2023.

- Persistent inflation, which was up 8.2% annually at the time of this writing

- Large hikes to the Federal Reserve’s fed funds rate, with further increases expected in 2023

- Global uncertainty caused by the continued conflict in Ukraine

- Volatility in global and U.S. stock markets

- Recessionary fears and economic uncertainty

- Continued supply chain disruptions and labor shortages

“It has been a dismal year for mortgage rates after record lows, with rates now soaring upward to over 7%,” says Brandon Boudreau, CEO of Alliance Title.

“Inflation has been the main culprit, with the Federal Reserve trying to combat it by raising key interest rates,” he explains, adding that “geopolitical events can have a strong effect, good or bad” when it comes to rate movements.

Find your lowest mortgage rate. Start here

What might cause mortgage rates to go down?

Mortgage rates are constantly in flux, and some recent increases have been followed by brief declines.

“In the near future, falling demand for mortgages may temporarily push down rates, but interest rates will otherwise remain high and tied closely to inflation,” says Dennis Shirshikov, a strategist for Awning.com and professor of economics and finance at City University of New York.

Unless the economy takes a major turn, experts aren’t expecting any massive or sustained drops in mortgage interest rates.

Inflation remains at the heart of the problem, according to Mike Hardy, managing partner at Churchill Mortgage. “If the collective market believes that the Federal Reserve will tame inflation, mortgage rates will begin to come down. But if the market does not have confidence, rates will stay in their current high range,” Hardy notes.

Expert mortgage rate predictions for 2023

To get a better idea of where mortgage rates may land throughout 2023, we surveyed a panel of lending and real estate professionals. Here’s a roundup of their rate predictions and trend analyses.

Keith Baker, Mortgage Banking program chair, North Lake Campus of Dallas College

2023 mortgage rate forecast: 9.31% (30-year), 7.93% (15-year)

What will drive mortgage rates in 2023?

“If central banks cannot get inflation down quickly, they will likely keep increasing interest rates on the short end and driving up deficit spending. There is also strong political and policy will to control inflation in the short-term,” says Baker.

“If the Federal Reserve’s rate hike program starts focusing on housing inflation, which accounts for about 40% of the key CPI metric, then rates might start coming down as home prices go down. At some threshold, if home prices come down enough, only a moderation of rate increases would allow home prices to rise, barring a recession.”

Advice to home buyers and homeowners

“If you need to buy right now, you should at least be able to lock in around 7%, with little likelihood of refinancing at lower rates for at least 18 months. Also, should prices continue to decline, waiting it out might mean adopting a more patient attitude. If you have stable employment and plan on staying in a home for at least five years, lock in now and wait until rates moderate before refinancing.”

“If you have stable employment and plan on staying in a home for at least five years, lock in now and wait until rates moderate before refinancing.”

–Keith Baker

Dennis Shirshikov, strategist at Awning.com and professor of economics and finance at City University of New York

2023 mortgage rate forecast: 9.25% (30-year), 8.75% (15-year)

What will drive mortgage rates in 2023?

“Continued inflation will drive rates up for the foreseeable future into 2023,” says Shirshikov. “Monetary tightening and the Federal Reserve raising its interest rate to combat inflation will also create additional upward pressure... I think that rates for 30-year and 15-year fixed-rate mortgages will be driven closer together as the long-term economic risk of recession increases and banks are less willing to lend.”

“Falling inflation and a huge drop in demand for mortgages could bring interest rates down significantly. The onset of a recession due to excessive monetary tightening could also bring down rates.”

Advice for home buyers and homeowners

“Refinance and purchase sooner rather than later if you plan on doing it at all.”

Brandon Boudreau, CEO of Alliance Title

2023 mortgage rate forecast: 7.5% (30-year), 7.0% (15-year)

What will drive mortgage rates in 2023?

“Runaway inflation could drive rates higher next year. Seeing rates double this year, no one should be surprised to see severe increases,” warns Boudreau. “There is also the very real possibility that the Fed will not lower rates, even with decreased inflation... There has been a large imbalance in housing supply and demand for quite some time, so this correction is somewhat needed for the long-term and is to be expected.”

“If the Fed is successful with its recent rate hikes, and geopolitical events do not worsen, I think we could see rates back in the mid-5% range in 2023 — maybe even in the first half of the year.”

Advice for home buyers and homeowners

“Supply will still be tough, and mortgage rates, even at today’s levels, remain good historically. We have been spoiled by such low rates in recent years, which has skewed expectations. I remain bullish on homeownership as rental inflation will remain high for quite some time.”

“If refinancing makes sense in the current environment, I would do so. If rates drop, you can always seek lender incentives and different terms to take advantage of them moving forward.”

“Mortgage rates, even at today’s levels, remain good historically. We have been spoiled by such low rates in recent years, which has skewed expectations.”

–Brandon Boudreau

Bruce Ailion, Realtor and real estate attorney in Atlanta

2023 mortgage rate forecast: 7.1% (30-year), 6.8% (15-year)

What will drive mortgage rates in 2023?

“Uncertainty about the future, particularly inflation, is driving the current 20-year highs for interest rates,” says Ailion. “However, rates can only increase so much before there is a collapse of the mortgage market and housing market. Significantly higher rates will predicate a far worse recession than the Federal Reserve would find acceptable.”

“Although we will have a recession in 2023, if we are not already in one, I expect that interest rates will remain high throughout most of the year. But as inflation moderates and the economy slows, interest rates should begin to decline.”

Advice for home buyers and homeowners

“Home buyers who plan to live in a home for several years can still purchase today with the plan to refinance when interest rates drop. Today’s buyer has the advantage of more homes on the market now than in the recent past and more negotiable sellers. The decline in competition likely offsets some of the recent increases in interest rates.”

Phil Greely, broker, Realogics Sotheby’s International Realty, Seattle

2023 mortgage rate forecast: 6.75% (30-year)

What will drive mortgage rates in 2023?

“Getting inflation under control is the top agenda of the Federal Reserve. [Its] only tool to make this happen is raising interest rates,” explains Greely. “This causes business-to-business borrowing to become more expensive, which will lead to higher unemployment. This will make short-term loans more expensive and, with a trickle-down effect, mortgage rates higher, too. We are in a rising interest rate environment for at least the next six months.”

“It’s possible that political pressure, a world war, or some other black swan event could cause the Fed to pivot. But until you see inflation reduce for several months, you likely won’t see rates go down much.”

Advice for home buyers and homeowners

“Home buyers need to purchase within their budgets, no matter what the rate is at the time they buy. It’s okay to purchase with an 8% rate, but you need to be able to afford that monthly payment without stress. This will mean you may have to buy less house than you could have a year ago.”

“Do not purchase with the expectation that you can refinance in a year, as a lower rate is not promised. Ensure you can afford your loan, regardless of the rate. Meanwhile, anyone refinancing right now needs to seriously consider why they are doing so. If you need to access equity for some reason, consider a home equity line of credit rather than a cash-out refinance.”

“If you need to access equity for some reason, consider a home equity line of credit rather than a cash-out refinance.”

–Phil Greely

Ralph DiBugnara, president of Home Qualified

2023 mortgage rate forecast: 5.75% (30-year), 5.06% (15-year)

What will drive mortgage rates in 2023?

DiBugnara explains that mortgage rates have been rising alongside the fed funds rate “in response to high inflation, increased consumer spending, and lower unemployment than expected. In turn, the market has seen a selloff of 10-year Treasury notes and an increase in rates on mortgage-backed securities.”

“Once the Federal Reserve stops raising rates... and we see consumer spending and employment reach market averages, we will start to see interest rates come down off these highs. Not only are mortgage rates up but the stock, equity, and bond markets are down a significant amount. Almost all of this is based on the uncertainty of what will happen next.”

Advice for home buyers and homeowners

“For borrowers right now, what’s most important is how the interest rate impacts your payment and if that payment meets your budget. Taking on high-interest credit card debt, which will only become much higher now, does not make sense compared to still very low mortgage rates. Keeping a definitive budget that meets your lifestyle should be the number one factor when considering locking in a rate now or refinancing.”

“For borrowers right now, what’s most important is how the interest rate impacts your payment and if that payment meets your budget.”

–Ralph DiBugnara

Mike Hardy, managing partner at Churchill Mortgage

2023 mortgage rate forecast: 5.375% (30-year), 4.875% (15-year)

What will drive mortgage rates in 2023?

“An under-tightening by the Fed or an unforeseen black swan event would cause mortgage rates to rise. The good news is that short of another major unforeseen event, I think we are close to the peak for mortgage rates,” says Hardy.

“Recessions are, by nature, deflationary. The Fed is in a tight spot, as [it needs] time to tame inflation while not stopping economic growth. But as we get deeper into a recession, we will see mortgage rates trend downward.”

Advice for home buyers and homeowners

“Unless there is a dire need for cash, I would wait to refinance for at least six to nine months, as I fully expect rates to trend down in 2023 while we endure this slowing economy in recession. A backup plan is to take a home equity line of credit and then restructure and consolidate any debt in 2023.”

Boyd Rudy, associate broker, Dwellings Michigan

2023 mortgage rate forecast: 5.0% (30-year), 4.5% (15-year)

What will drive mortgage rates in 2023?

Rudy emphasizes that Federal Reserve policy decisions, inflation, and unemployment can all affect mortgage rates. “Then there are the current housing market and demand for mortgages to consider. If more people are looking to purchase or refinance homes, this can drive up rates as lenders become more competitive for business.”

“A potential decrease in inflation could lead to lower interest rates. Additionally, if the job market continues to improve and the economy sees sustained growth, this could also drive rates down. On the policy side, actions taken by the Fed can have a significant impact, as well.”

Advice for home buyers and homeowners

“Do your research and consider all your options before making a decision. It may be tempting to lock in an interest rate now before rates go higher, but it’s important to ensure you have found the perfect property for you and can afford the monthly payments.”

“Waiting a little longer for the right house could end up saving you money in the long run. For those seeking to refinance, carefully consider whether or not will save you enough money to justify the fees and closing costs. It may be more beneficial to wait until interest rates drop lower or until you improve your credit score.”

Time to make a move? Let us find the right mortgage for you