The Refi Boom’s Second Wave has begun, and 5-year ARMs are leading the charge.

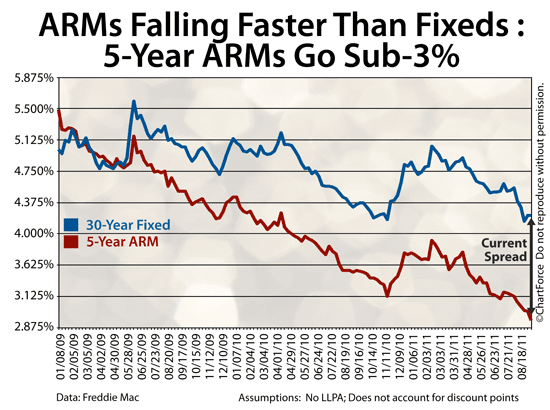

5-Year ARMs Fall Below 3 Percent

The 5-year ARM is cheap right now. With the global economy sagging and outcomes uncertain for 2011 and 2012, investors have embarked on a massive flight-to-quality.

Wall Street traders are ditching risky assets and moving into “safe” ones — a class which includes U.S. mortgage-backed bonds. As a result, bond prices are way up this year, and as recently as last week, economic weakness re-sparked a rally.

The U.S. jobs market turned up zero new jobs in August and, joining Greece, Italy is generating some sovereign debt concerns. Long-term, markets expect a turn-around. Near-term, however, not so much.

Mortgage rates have tumbled. Assuming 0.6 discount points, ARMs are now below 3 percent.

Click here to for an ARM rate quote

.

The 5-Year ARM Is At Historically-Low Levels

Mortgage rates have been falling for 5 months. Rates on 5-year ARMs, though, have out-fallen those for other products including both the 30-year fixed rate mortgage and the 15-year fixed rate mortgage.

As an illustration, the start of the 2011 Refi Boom in mid-April 2011 :

- The 30-year fixed is down 0.69 percent

- The 15-year fixed is down 0.74 percent

- The 5-year ARM is down 0.82 percent

Meanwhile, the relative drop in the 5-year ARM has made it a bargain for families that know they’re moving in fewer than 5 years, or that are comfortable with a non-fixed mortgage rate.

Click here to for an ARM rate quote

.

Is The 5-Year ARM Right For You?

A $300,000 5-year ARM mortgage will save your $223 monthly over a comparable 30-year fixed. That’s big savings. But just because the 5-year ARM is cheaper, that doesn’t make it right.

ARMs carry interest rate adjustment risk, for one, and should only be selected after careful consideration. Talk to your lender about adjustable-rate mortgages and whether they’re right for you.

Time to make a move? Let us find the right mortgage for you

.