Is there a VA loan income limit?

Some mortgage programs, like the USDA loan, come with a top income limit. But there’s no income limit for VA borrowers.

You could earn $1 million per year and the program is still open to you.

That said, the Department of Veterans Affairs (VA) has a unique and unusual way of looking at income. Instead of the total number, it’s most interested in “residual income,” the cash you have left over after all major expenses. There is a minimum based on family size and location.

When lenders look at loan applications they typically have several major items to check: credit, debts, the amount down and income. In each case, the VA approach to these issues is different from other loan products – but different in a way which very much benefits borrowers.

Ready to check your VA loan eligibility? Start here.Residual income required for a VA loan

The VA will only guarantee so much financing.

VA lenders are interested in such things as credit, debts and the amount down but they also want to know about residual income, the amount of cash available after monthly expenses.

This is a safeguard that is not established for any other loan type. The VA wants to make sure that veterans don’t get “in over their heads” with a too-big mortgage. There must be a minimum amount left over every month to pay for family expenses...you know, somewhat important things like food and gasoline.

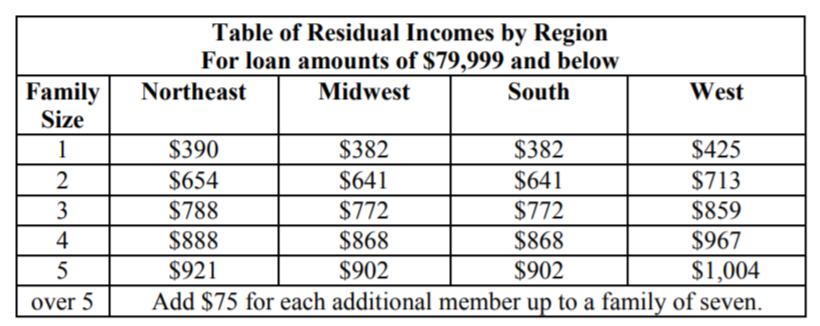

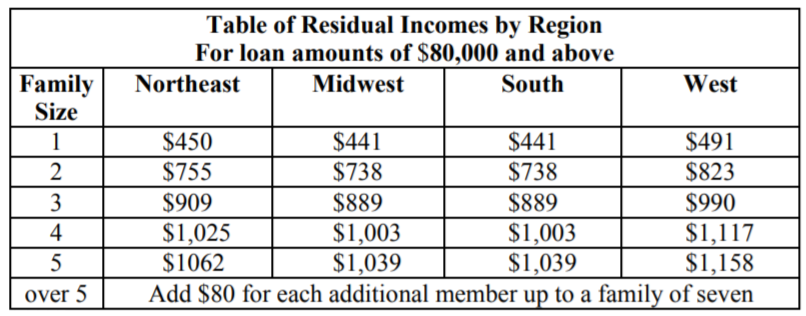

The residual income is calculated by looking at family size, loan amount (more or less than $80,000), and location. The VA charts below show how much residual income you need depending on your particular situation.

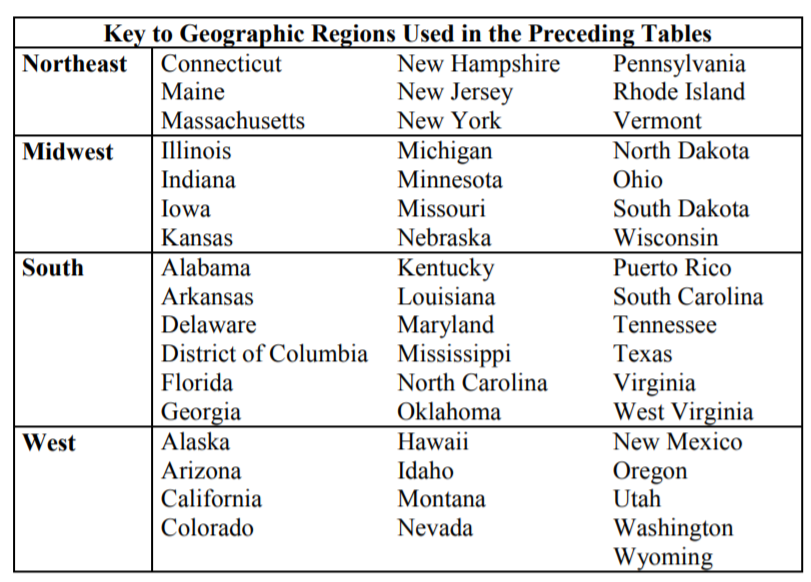

The definitions of geographic areas according to the VA look like this.

The real importance of the residual income system is it prevents home buyers from borrowing more mortgage money than they should, from becoming house poor. In turn, with more comfortable monthly finances borrowers represent less risk. This shows up in delinquency rates — the VA program delinquency rate is less than half the rate for FHA financing according to the Mortgage Bankers Association.

Credit scores & VA loan income eligibility

Home buyers usually assume there’s a minimum score to qualify for a mortgage. Not so for the VA loan. There’s no stated required credit score in the VA lending manual.

The VA explains that it has “no minimum credit score requirement; instead VA requires a lender to review the entire loan profile to make a lending decision.”

The VA does not lend money, it’s actually a loan-guarantee program. If something goes wrong — if you don’t pay your mortgage — the VA will step in and make up some or all of the lender’s loss.

In theory you can have a 400 credit score and still get a VA-backed mortgage.

In practice, that’s hugely unlikely to happen. Instead, each lender has a different risk appetite. Under the VA program lenders can establish the credit level they will accept, maybe 620 for Lender Smith and 640 for Lender Jones. Because credit requirements can differ it pays to shop around for VA financing.

Debts

One of the major measures used by lenders when considering mortgage applications is the debt-to-income ratio or DTI. There are really two DTI measures, a “front” ratio and a “back” ratio. The front ratio compared housing costs such as mortgage principal, mortgage interest, property taxes, and property insurance (PITI to lenders) to your gross monthly income — the income you earn before taxes. For instance, if your monthly housing costs are $1,620 and you have a gross monthly income of $6,000 your front ratio is 27%.

The back ratio include housing costs plus monthly expenses for such things as credit card payments, student loans and auto financing. If the combined expenses amount to $2,400 then the back ratio is 40%. The result of looking at the front and back ratios would be 27/40.

Different loan programs have different basic DTI ratios.

- Conventional – 28/36

- FHA – 31/43

- USDA – 29/41

- VA – 41/41

DTI ratios can be higher for borrowers with compensating factors such as strong cash reserves, an energy-efficient home or additional income such as overtime or bonus money.

If you look at the DTI ratios for different programs you can see something strange. The VA DTI ratio is 41/41 — the same number twice. How come?

If you borrow with most loan programs the front ratio is fairly set, there is only so much you can spend on housing from your gross monthly income. However, with VA loan income eligibility if you have few monthly debts to pay — or no monthly debts to pay — then you can borrow more for housing costs, perhaps up to 41% if your lender allows it.

All the more reason to pay off credit cards, student loans, and car loans if you’re having a hard time qualifying for a big enough VA home loan.

Amount down

With the VA you can obtain 100% financing. The cost of the home can be the mortgage amount. Buy a home for $300,000 and you can borrow $300,000. This happens because lenders will accept the VA guarantee in lieu of a down payment.

You still owe the full amount. But you don’t have to come up with 20% down that conventional loans require to avoid mortgage insurance, or even the 3.5% down that FHA requires.

But even though you can buy with nothing down through the VA program you can’t just borrow any amount. The VA has a way to limit the amount it will guarantee, what is known as the “residual income” test.

Check your eligibility for a VA loan

If you have military experience, current or former, you may be eligible for a zero-down home loan via the VA loan.

Check rates and get an eligibility check at the link below.

Time to make a move? Let us find the right mortgage for you