Don’t Neglect An Exit Strategy When You Borrow With A HELOC Or Home Equity Loan

When you cash out some of your home equity, chances are you concern yourself mainly with the interest rate and loan costs. That’s the smart way to shop. But one thing can really affect your finances at a later date. Lenders don’t mention it, and borrowers sure don’t ask about it.

This Term That Must Not Be Named is called “subordination.”

Verify your new rateCheck Your Dictionary: “Subordination” Is Weakness, Servitude, Helplessness

Okay, so your second mortgage is not likely to tie you up and tickle you until you cry. But it can make you weep with frustration if you decide that you want to refinance your first mortgage, and your HELOC or home equity lender decides to give you a hard time about it.

What Is Second Position?

It’s not ballet. It’s a mortgage thing.

Mortgage subordination (second position) works like this.

Supposed you borrowed $300,000 to purchase a $400,000 house. You put $100,000 down, your lender threw roses and money at you and everyone rejoiced.

And then a few months later, you wished you had some of that $100,000 back. Something about one kid in grad school and the other wanting an expensive wedding. You apply for a home equity line of credit to get back $60,000 of that deposit. So you’d owe $360,000 for your $400,000 house, or 90 percent of its value.

That second mortgage takes what’s called “second position,” behind the first mortgage. This means that if you have a midlife crisis, run off to Tahiti and abandon your house and bills, the first lender (aka, “senior lienholder”) gets repaid first from the proceeds of the foreclosure sale on your property.

The home equity lender gets paid from the leftovers, and that’s often not enough.

That’s why interest rates are higher for second mortgages — their chances of twisting in the wind after a foreclosure are much higher.

This “back of the line” position is called “subordination.” The interests of the home equity lender (also called the “junior lienholder”) are “subordinate” to those of the first mortgage lender.

Verify your new rateWhen Subordination Becomes Helplessness

Everything’s fine, your student gets straight A’s, your daughter’s still married, and mortgage rates drop about one percent less than you’re paying for your first mortgage (the $300,000 loan).

Your credit is awesome, lenders still love you, and you could save a ton by refinancing the first mortgage. But now, your first and second mortgage together total 90 percent of your property value.

That means you’ll have to pay private mortgage insurance premiums if you refinance both loans into a new first mortgage, or you’ll have to refinance the first mortgage and leave the second one alone.

To do this, the junior lienholder must agree to subordinate its interest to that of the new lender.

That should simply be formality in which the home equity lender informs your title company that it will remain in second position. Without this document, the old lender moves into first position, and your new refinance would take second position.

Except it won’t, because no lender would be willing to take second position while charging the rates of a first-position loan. That would be stupid.

Some Home Equity Lenders Are Not Helpful

Should be a no-brainer, right? Subordination has exactly no effect on the second lender’s position.

But some lenders are, for lack of a better term, jerks. They refuse to subordinate.

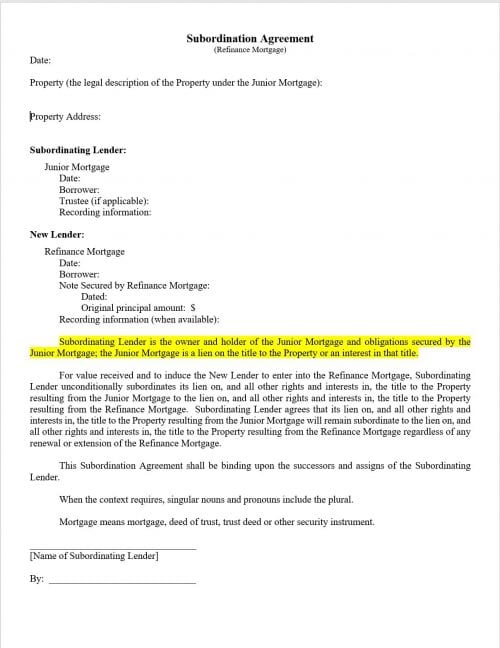

And that’s why borrowers should ask to see the home equity lender’s written subordination agreement and policy before agreeing to borrow.

Here is a sample provided by Freddie Mac:

Common requirements for subordination approvals include minimum credit scores and maximum CLTV (combined loan-to-values). You may be able to secure a subordination by paying down the balance of a home equity loan or reducing your available credit on a HELOC.

Of Course, No One DOES This: What Now?

Stock kicking yourself. It hurts, and it doesn’t work. First, try having a conversation with your home equity lender. A written note (or Tweet, or whatever), explaining your position can’t hurt. Especially if your property value has increased, your credit rating is excellent and you have never missed a payment to this lender.

Mention that you can always refinance out of that loan to another more congenial lender.

Next, follow up. Refinance to a lender that has a policy of allowing subordination. Mention this when you apply - that you have no intention of doing an early payoff and want to be sure that you can subordinate.

Then, you can subordinate your new second mortgage to your new refinance.

What Are Today’s Mortgage Rates?

Today’s mortgage rates have dropped a bit since the 2016 election cycle. This may out you in a good position to lower your rate and payment, replace an ARM with a fixed loan, or just pull more money from your home equity.

Time to make a move? Let us find the right mortgage for you