Mortgage payment: Your biggest expense

You can clip coupons to reduce grocery bill. You can bring a bag lunch to work. And you can skip your daily latte to tweak your budget. But the biggest bite out of your paycheck is probably your mortgage payment.

Whether you are about to buy your first home, or are years into making mortgage payments, there are steps you can take to keep your mortgage payments low even when interest rates rise.

Verify your home buying eligibility9 strategies to reduce your mortgage payment

While not all of these apply to every loan scenario, and some require a cash outlay, one of these may work for you. Note that some strategies can increase your total loan costs while dropping your payment.

1. Buy a cheaper house

The smartest move you can make before you buy a home is to establish your own limit on your monthly housing payment. Don’t forget to include your principal and interest, taxes and homeowner’s insurance, plus possibly mortgage insurance and an HOA fee.

Sticking to that monthly mortgage payment figure could mean you need to lower your expectations a little once you start looking at homes. However, it’s far better to “under-buy” and move up later than to “over-buy” and struggle to make your payments.

2. Increase your down payment

Your down payment impacts your payment a great deal. If you buy a $400,000 house and put $40,000 down (10 percent), your principal and interest is $1,719. That’s with a 30-year fixed-rate loan at 4.0 percent.

But wait; there’s more — you’ll also pay private mortgage insurance (PMI). With a 700 FICO score, that’s another $180 a month. If you have the cash to make a 20 percent down payment, your payments drop by nearly $200 per month. And you can skip paying PMI, saving nearly $400.

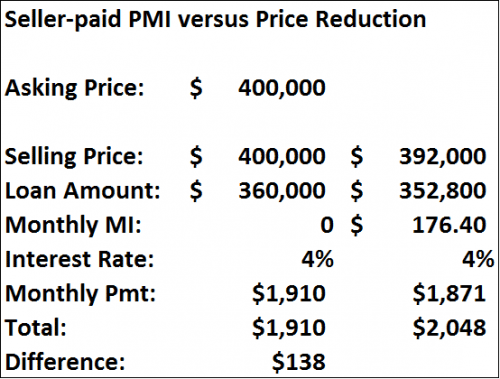

3. Have your seller pay your PMI

Even if you don’t have the cash to make a larger down payment, you can reduce your monthly housing bill with upfront PMI. Ask your home seller to pay this instead of asking for a price reduction. Seller-paid closing costs can reduce your monthly outgo a lot more than a price reduction in the same amount.

For instance, in the example above, you could purchase a single-premium MI policy for about two percent of the loan amount, or $7,200. By asking the seller to cover this instead of reducing the property price, you save significantly more over the life of the loan.

4. Pay points

You can “buy down” your interest rate by paying points at your closing. By paying one or more points, each equal to one percent of your loan balance, you can reduce the mortgage rate on your loan.

Ordinarily, one point drops your 30-year fixed rate by .125 to .25 percent. But with a 5/1 or 3/1 ARM, you’ll get a much larger reduction.

That’s help you might be able to get from the seller. The amount of concessions you’re allowed to have depend on the loan program, FHA, for instance, allows up to six percent of the loan amount.

Verify your home buying eligibility5. Drop mortgage insurance coverage

If you already own your home and are looking for a way to reduce your monthly payments, see how close you are to eliminating your PMI.

According to the Consumer Financial Protection Bureau, your PMI payments stopped when you reach the date specified on your PMI disclosure papers. It should be the month that your loan balance drops to 80 percent of your original home value.

When your loan-to-value reaches 78 percent, your PMI should go away automatically, as long as your payments are up-to-date.

You can also ask to have your PMI eliminated if you have made extra payments to reduce your loan balance below 80 percent of your home’s original value.

Finally, some lenders allow you to drop coverage if you pay for an appraisal to prove that you have more than 20 percent in home equity.

6. Recast your loan

Although most lenders don’t actively market this service, you can request a loan “recast” or “re-amortization.”

You do this by making a lump sum principal payment, reducing the principal balance. Then the lender recalculates your payment based on the lower balance.

Recasting makes sense if the terms of your loan are better than what’s currently available.

7. Refinance

Refinancing your loan instead of recasting costs a bit more, but you could end up with even lower monthly payments depending on your interest rate and your loan term.

Refinancing lowers your payment in two ways – first, by lowering the interest rate, and second, by re-amortizing your remaining balance over a new loan term.

Verify your home buying eligibility8. Request a new tax assessment

Part of your loan payment includes your property taxes. If you think your assessment is too high, you can appeal it to reduce your tax burden. But be careful: a new assessment could find that your home is worth more than before and your taxes could go up.

9. Choose an ARM

Most new homeowners don’t keep their first real estate purchase more than a few years. So why pay for a 30-year fixed-rate you won’t use? The 7/1, 5/1 and 3/1 hybrid ARM products offer fixed introductory rates. These rates can be .5 percent to 1.25 percent lower than the 30-year rate.

With a $300,000 loan, your payment would be as follows with one national lender’s current rates:

- 30-year fixed at 4.00 percent: $1,432

- 7/1 ARM at 3.75 percent: $1,389

- 5/1 ARM at 3.25 percent: $1,306

- 3/1 ARM at 3.00 percent: $1,265

So the ARM could shave up to $167 a month from your payment in this case.

What are today’s mortgage rates?

Current mortgage rates are still low, although they are expected to increase in 2017. To get the lowest payment, choose a loan with a low rate (this may not be a fixed-rate mortgage), shop aggressively, and do it soon before interest rates move higher.

Time to make a move? Let us find the right mortgage for you