Open Up Financing Opportunities By Improving Your Credit

If you have a poor credit score, you probably know it. And you’d probably like to improve it.

It’s not that hard to raise your credit score; a few changes can make big differences.

Erroneous items, paid-off debt — they can drag down your score undeservedly.

The first step to go from poor to fair credit is to find out why your credit score is low, and how to make it better.

Thousands of mortgage shoppers are doing that daily. You can be one of them.

Verify your new rateWhat’s The Difference Between Poor Credit And Fair Credit?

There’s no standard definition of fair credit or poor credit, but there are some ranges in common use.

“Poor credit” usually means having a FICO score under 620 — the level at which many lenders set their minimum acceptable score. “Fair credit” is often defined as 620 to 679.

Currently, the average FICO score in the U.S. is 685, according to Governing Magazine, which is slightly above the “fair” range.

The High Cost Of Low FICO Scores

Low or subprime credit scores can suck a lot of money out of your bank account. When you have fair credit, you pay much less in loan fees and interest charges than you do with poor credit.

One online credit tool indicates that a 37-year-old woman in California would pay $131,000 more in financing costs over her lifetime with poor credit than she would with fair credit. That’s 131,000 reasons to raise your credit score.

The disadvantages don’t end there, however. People with low FICO scores have difficulty with:

- Renting: Landlords check your credit before deciding to rent to you, and they may decline your application or increase your deposit

- Buying insurance: In most states, insurers are allowed to consider your credit score when setting your rate

- Employment: Employers can check your credit before deciding to hire you

How Bad Credit Happens To Good People

Many factors contribute to low FICO scores – examples include a short or limited credit history (aka “thin file”), high account balances, too many accounts, or too many credit applications (inquiries).

The most damaging stuff in your file, though, is likely to be found in your history — missing or past due payments. Here are the five most common reasons for low credit scores, according to FICO:

- Serious delinquency

- Serious delinquency with public record or collection filed

- Time since delinquency too recent

- Number of accounts with delinquency

- Proportion of balances to credit limits on revolving accounts is too high

Each scenario is reversible, but some take longer to fix than others.

How To Raise Your Credit Score

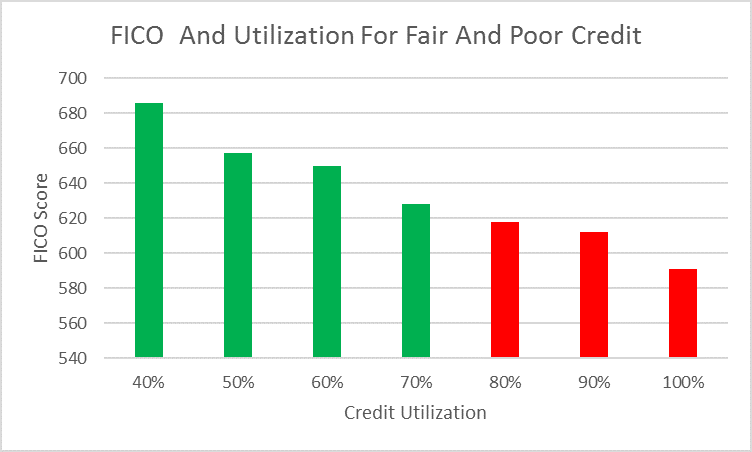

Notice that four of the top five reasons for low credit scores contain the word “delinquency.” The fifth one is related to the amount of available credit that you’re actually using — your “utilization ratio.”

Utilization ratio is the comparison between your available credit and amount borrowed.

You have a ratio of 50% if you $10,000 in available credit, and have charged $5,000. Keep your utilization ratio below 30% for better scores, says credit bureau Experian.

If your credit score is “poor” for any of the reasons mentioned above, there is good news — they can be fixed, and you may be able to go from poor to fair in just a few months.

Verify your new rateFix Your Credit History

On-time payments are the only way to overcome a bad history and raise your credit. To the credit bureaus, “on time” means within 30 days of the due date.

If you have trouble remembering to pay your bills, try setting up automatic payments from your checking account so that you don’t miss a payment.

If you have collection accounts that are fairly recent (less than two years old), contact the agency about paying them – and try to get them to agree to remove the derogatory entry from your credit report. They may tell you they can’t do this, but in fact they can.

Older collections don’t do as much damage as newer ones, and in fact, paying them can move them into the present and cause your credit score to drop.

Again, the best way to pay them and impact your score in a positive way is to persuade both the collection agency and the original creditor to remove the negative information from your credit report in exchange for your payment-in-full.

Too Much Debt

The fifth top cause of low credit scores is using too much of your available credit.

This is a big deal because maxing out credit lines is a red flag to creditors — your spending habits are unsustainable. Continue spending more than you earn and you’re likely to default or file bankruptcy.

On average, people with credit scores under 620 use more than 70 percent of their available credit, while those with fair credit use 40 to 70 percent. In general, the lower your utilization, the better your score.

If you have $2,000 in available credit, and you’ve got a $1,750 balance, your utilization is very high — $1,750 divided by $2,000 = 87.5 percent. Your goal should be to pay it down to $1,200 or less.

How To Reduce Your Utilization

You may be able to quickly lower your utilization ratio by consolidating your debt with a personal loan or home equity loan — replacing credit card balances with a new installment account or mortgage.

However, this strategy fails about 75 percent of the time because most people with credit problems don’t stop overspending. Only try this if you know you’ll pay off your consolidation loan every month on time and that you won’t carry a balance on your credit cards again.

The more reliable method is to stop charging on your cards and pay as much each month as you can afford — no more coasting on that minimum payment.

You Can Raise Your Credit Score

Bad credit doesn’t usually happen overnight, and it doesn’t go away overnight either. But you can raise your credit score from poor to fair in months if you make the effort.

Plan to motivate yourself by monitoring your credit score and accounts as you take control. Watching your FICO score increase month after month feels great.

What Are Today’s Fair Credit Mortgage Rates?

Mortgage rates for fair credit aren’t as good as those for people with good or excellent credit. However, the current economic situation has made these loans highly affordable.

Time to make a move? Let us find the right mortgage for you